The 69% Reality: What It Means to Build a Career in a Streaming-Dominated Market

The global recorded music business is no longer transitioning into the streaming era. It is fully inside it.

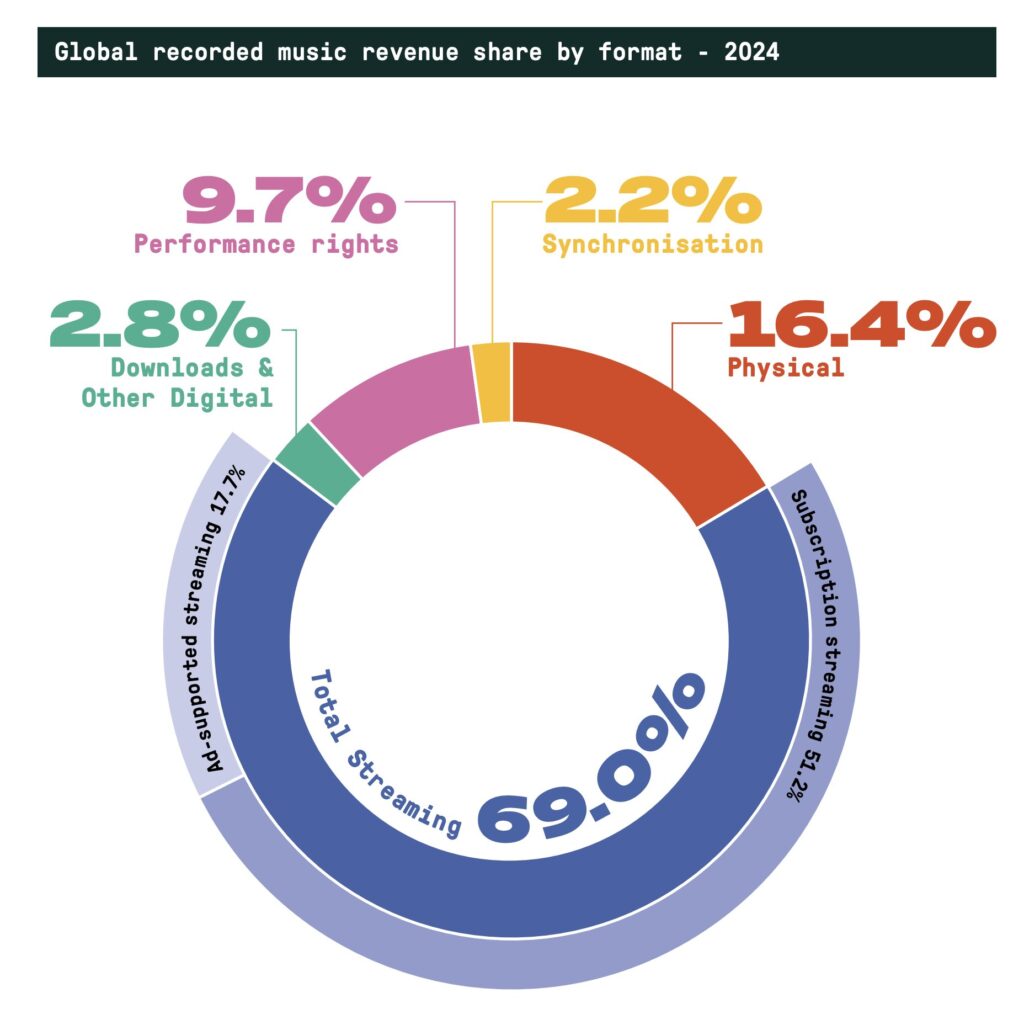

According to the IFPI Global Music Report 2025 (State of the Industry), streaming accounted for 69.0% of total global recorded music revenues in 2024, generating more than US$19 billion worldwide. This marks the tenth consecutive year of industry growth and confirms that streaming is not merely the dominant format, it is the structural foundation of the modern music economy (IFPI, 2025).

But dominance brings consequences.

If nearly 70% of all revenue flows through streaming platforms, what does that mean for artists trying to build sustainable careers, especially independent ones?

Streaming Is the Industry

The Structural Numbers

The IFPI report outlines the global revenue breakdown for 2024:

- Streaming: 69.0%

- Physical formats: 16.4%

- Performance rights: 9.7%

- Downloads & other digital: 2.8%

- Synchronisation: 2.2%

Total global recorded music revenues grew again in 2024, extending a decade-long recovery driven overwhelmingly by subscription streaming.

In practical terms, this means:

- Your primary revenue exposure is platform-based.

- Your visibility is algorithm-mediated.

- Your financial sustainability depends on digital consumption patterns.

The “market” is no longer retail. It is behavioral data.

Subscription Growth and Its Implications

Paid Streaming Drives the Engine

The IFPI report notes that paid subscription streaming remains the largest contributor to streaming revenue growth globally. Hundreds of millions of users worldwide now pay monthly subscription fees for access to catalog-based listening.

This means subscription revenue:

- Is more stable than ad-supported streaming.

- Rewards catalog depth.

- Incentivizes long-term listening behavior.

For independent artists, this creates both opportunity and structural pressure.

If revenue flows through subscription pools, your share depends not on price per unit sold, but on share of total listening time within massive ecosystems.

The Algorithmic Economy

Exposure Is Not Neutral

In a streaming-dominated market, discovery is platform-curated.

Playlists, editorial and algorithmic, function as gatekeepers. Recommendation engines shape listening habits. Engagement metrics influence future visibility.

This transforms artistic strategy.

In the physical era:

- You sold ownership.

In the streaming era:

- You compete for recurring attention.

That difference is existential.

Music is no longer a product purchased once. It is a service consumed continuously.

Artists must think in terms of:

- Release cadence

- Retention

- Listener conversion

- Catalog sustainability

The streaming market rewards consistency more than sporadic brilliance.

Revenue Per Stream vs Revenue Share

The Misunderstood Debate

The common public debate focuses on “per-stream payouts.” But the IFPI report emphasizes a broader economic structure: streaming operates under a revenue-share model.

Platforms distribute revenue based on total consumption share, not fixed unit pricing.

This means:

- The more total listening occurs globally, the larger the revenue pool.

- But your percentage share determines your income.

As global streaming expands, particularly in emerging markets, total revenue grows. Yet competition intensifies proportionally. To put it in simple words, streaming services (based on their claims) count the number of all the streams in each month and then divide their total revenue (after reducing the service fees and etc) by that number, the result is the pay per stream for your music in that month.

Global Expansion: Growth Beyond the West

One of the most important insights from the IFPI 2025 report is that all global regions experienced revenue growth for the fourth consecutive year.

Streaming growth is no longer confined to North America and Western Europe. Rapid development is visible in:

- Latin America

- Sub-Saharan Africa

- Middle East & North Africa

- Asia

This global expansion shifts career strategy for independent musicians.

It is no longer sufficient to think locally.

Metadata, language accessibility, cross-border marketing, and cultural positioning become decisive factors in global discoverability.

Artists building careers today must think internationally from day one.

The Psychological Impact on Artists

Metrics as Identity

Streaming platforms provide real-time metrics:

- Monthly listeners

- Follower counts

- Save rates

- Skip rates

- Completion rates

These numbers can easily become proxies for artistic worth.

But data visibility creates volatility in creative psychology.

A physical album that sold modestly could still feel meaningful.

A streaming release that performs “below algorithmic expectation” feels instantly public.

Career building in a streaming-dominated market requires emotional resilience as much as musical craft.

The Disappearance of Ownership Culture

From Albums to Access

Physical revenue declined by 3.1% globally in 2024, according to IFPI. Downloads represent just 2.8% of total revenue.

Ownership has become secondary.

Access is the primary consumer behavior.

For album-oriented artists, this presents a strategic dilemma:

- Do you adapt to playlist culture?

- Or double down on narrative, long-form releases?

The answer may not be binary.

Streaming rewards frequent engagement, but catalog depth drives long-term accumulation.

Artists who build coherent bodies of work, not just singles, may benefit more as subscription ecosystems mature.

Diversification Is No Longer Optional

If 69% of revenue comes from streaming, 31% does not.

Performance rights grew in 2024. Synchronisation grew. Live sectors (outside the recorded market) remain powerful income drivers.

The artists who will sustain careers are those who:

- Leverage streaming for exposure.

- Monetize performance rights effectively.

- Develop sync relationships.

- Build live audiences.

- Maintain catalog strategy.

Streaming is the foundation, but it should not be the only pillar. Or better to say, it can not be the main pillar.

Long-Term Career Architecture

Catalog as Infrastructure

In a subscription world, older recordings continue generating revenue as long as they are streamed.

Unlike physical inventory, digital catalog does not expire.

This makes long-term artistic thinking crucial.

Every release becomes part of a permanent ecosystem.

The streaming-dominated market rewards:

- Consistency

- Depth

- Identity clarity

- Global accessibility

- Rights ownership

Short-term viral moments rarely translate into structural careers without infrastructure behind them.

The 69% Streaming Reality in a Nutshell

Streaming dominance is not temporary. It is the defining economic structure of the contemporary music industry.

According to IFPI 2025:

- Streaming generated over US$19 billion.

- It represents 69% of recorded revenue.

- The industry has grown for ten consecutive years.

For independent artists, this means:

- You are building inside a platform economy.

- Visibility is algorithmically shaped.

- Revenue is share-based, not unit-based.

- Global markets matter more than ever.

- Diversification determines resilience.

The streaming era does not eliminate artistic ambition, but it demands strategic literacy.

To build a career today is not merely to compose or record. It demands much more.

And in a market where 69% of revenue flows through streaming platforms, ignoring that reality is no longer an option.

#MusicIndustry #StreamingEconomy #GlobalMusicReport #IndependentArtists #MusicBusiness #DigitalAlbum #StreamingStrategy #MusicRevenue #ArtistCareer #MusicMarket #SubscriptionStreaming #Tunitemusic

Photo: IFPI Global Music Report 2025